Starting a business in the UAE is exciting—fast growth opportunities, a global market, and a business-friendly ecosystem. But along with these advantages comes a crucial responsibility: understanding Value Added Tax (VAT).

For startups, VAT isn’t just a compliance requirement—it’s a financial system that, when managed correctly, can support smoother operations and smarter decision-making. At Bookkeeping Expert, we simplify VAT so you can focus on building your business.

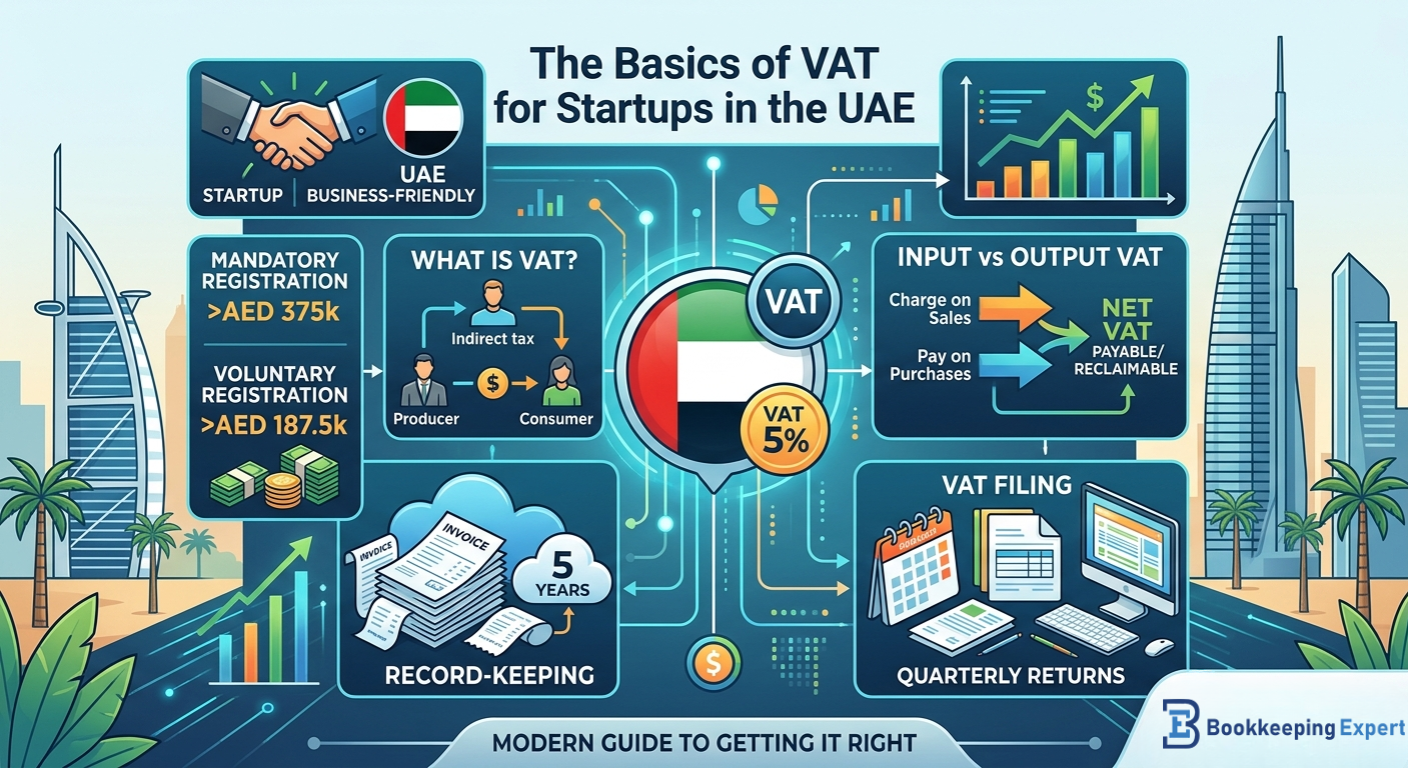

What is VAT and Why Does It Matter?

Value Added Tax (VAT) is an indirect tax applied to most goods and services in the UAE. Introduced in 2018 at a standard rate of 5%, VAT has become a core part of the country’s financial framework.

Why startups should care:

-

It impacts pricing strategies

-

Affects cash flow

-

Requires accurate record-keeping

-

Non-compliance leads to penalties

Understanding VAT early prevents costly mistakes later.

Do You Need to Register for VAT?

Not every startup must register immediately—but knowing the thresholds is key.

VAT Registration Types:

-

Mandatory Registration: If annual taxable turnover exceeds AED 375,000

-

Voluntary Registration: If turnover exceeds AED 187,500

Startup Insight: Even if you're below the mandatory threshold, voluntary registration can enhance credibility and allow input tax recovery.

Understanding Input VAT vs Output VAT

VAT works on a simple principle, but it’s often misunderstood.

-

Output VAT: Tax you charge customers on sales

-

Input VAT: Tax you pay on business purchases

Your obligation: Pay the difference to the government.

Example:

If you collect AED 5,000 in VAT and pay AED 3,000 on expenses, you remit AED 2,000.

VAT Filing: What Startups Need to Know

VAT-registered businesses must file returns regularly (usually quarterly).

Filing includes:

-

Total sales and purchases

-

Output VAT collected

-

Input VAT paid

-

Net VAT payable

Pro Tip: Late or incorrect filings can result in penalties—automation and professional support can help avoid this.

Record-Keeping: Your Compliance Backbone

The UAE requires businesses to maintain proper financial records for at least 5 years.

Essential records include:

-

Tax invoices

-

Receipts

-

Credit notes

-

Import/export documents

Modern Approach: Use cloud accounting tools to keep everything organized and audit-ready.

Common VAT Mistakes Startups Should Avoid

Even promising startups can struggle with VAT if not careful.

Watch out for:

-

Missing registration deadlines

-

Incorrect invoicing formats

-

Claiming ineligible input VAT

-

Ignoring reverse charge mechanisms

Avoiding these pitfalls keeps your business safe and efficient.

How VAT Impacts Your Pricing Strategy

VAT directly affects how you price your products or services.

You need to decide:

-

Will your prices be VAT-inclusive or exclusive?

-

How will VAT affect competitiveness?

Smart Move: Transparent pricing builds trust with customers and avoids confusion.

VAT and International Transactions

If your startup deals with imports, exports, or cross-border services, VAT rules become more nuanced.

Key considerations:

-

Zero-rated exports

-

Reverse charge mechanism on imports

-

Place of supply rules

Understanding these ensures compliance while optimizing tax benefits.

Why Startups Should Consider VAT Experts

VAT compliance can be complex, especially when you’re focused on growth.

Working with experts helps you:

-

Stay compliant with UAE regulations

-

Avoid costly penalties

-

Optimize tax efficiency

-

Focus on scaling your business

At Bookkeeping Expert, we provide tailored VAT solutions designed specifically for startups navigating the UAE market.

Final Thoughts

VAT might seem like just another regulatory requirement, but for startups in the UAE, it’s a critical part of building a sustainable and compliant business.

The earlier you understand and implement the right VAT practices, the smoother your growth journey will be.

Let VAT work for you—not against you.