Dubai has long been known as a global business hub with a tax-friendly environment. However, with the introduction of corporate tax regulations in the UAE, the financial landscape has entered a new era—one that requires businesses to be more structured, transparent, and compliant than ever before.

The key question every business owner should be asking today is simple: Are you truly prepared for corporate tax compliance in Dubai?

Understanding the Shift in UAE Tax Landscape

The UAE’s introduction of corporate tax marks a significant transformation in how businesses operate. While the rates remain competitive globally, compliance requirements demand attention to detail and financial discipline.

This shift means businesses must now focus on:

-

Accurate financial reporting

-

Proper documentation of income and expenses

-

Timely tax filings

-

Clear audit trails

Ignoring these responsibilities is no longer an option.

Why Corporate Tax Compliance Matters More Than Ever

Corporate tax compliance is not just about paying taxes—it’s about building financial credibility and avoiding penalties.

Non-compliance can lead to:

-

Financial penalties and fines

-

Legal complications

-

Reputational damage

-

Operational disruptions

On the other hand, strong compliance improves business transparency and investor confidence.

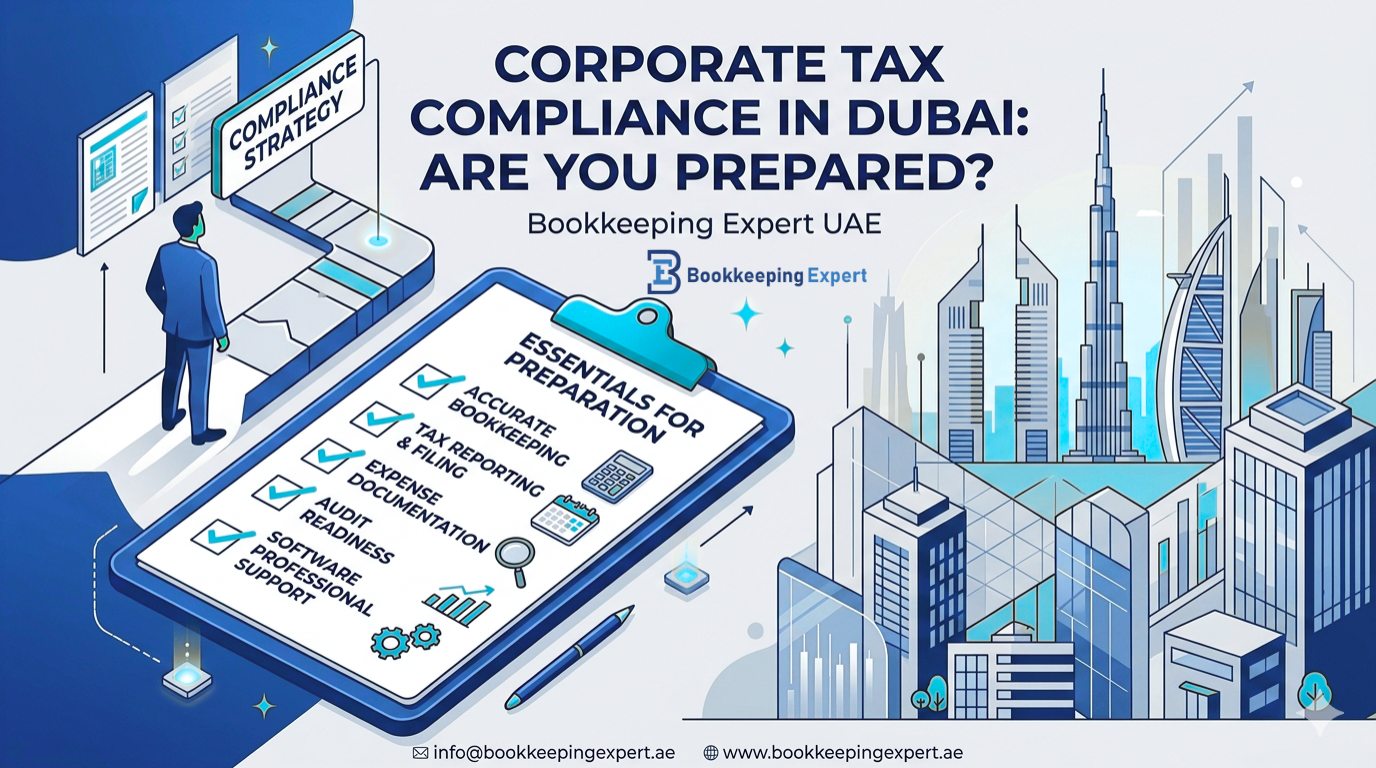

Key Areas of Corporate Tax Compliance in Dubai

To stay compliant, businesses must focus on several core areas:

1. Accurate Financial Records

Maintaining clean, organized financial statements is essential. Every transaction must be properly recorded and categorized.

2. Proper Income Reporting

All revenue streams must be declared correctly, including cross-border and digital income sources.

3. Expense Classification

Only eligible business expenses should be deducted, supported by valid documentation.

4. Timely Filing

Missing deadlines can result in penalties, making scheduling and planning critical.

5. Audit Readiness

Businesses must always be prepared to justify financial records if reviewed by authorities.

Common Compliance Challenges Businesses Face

Many businesses in Dubai are still adjusting to corporate tax requirements. Some common challenges include:

-

Lack of awareness about tax rules

-

Poor bookkeeping practices

-

Incomplete financial documentation

-

Misclassification of expenses

-

Inadequate internal controls

These issues often lead to unnecessary risks and compliance gaps.

How to Prepare Your Business for Corporate Tax

Preparation is the key to avoiding stress and penalties. Businesses can take proactive steps such as:

Strengthen Bookkeeping Systems

Ensure all financial transactions are recorded accurately and consistently.

Implement Accounting Software

Automated systems reduce human error and improve reporting accuracy.

Separate Personal and Business Finances

This is essential for clear tax reporting and audit protection.

Review Financial Statements Regularly

Monthly or quarterly reviews help identify issues early.

Work with Tax Professionals

Expert guidance ensures compliance with evolving UAE tax laws.

The Role of Professional Accounting Support

Corporate tax compliance requires more than basic bookkeeping—it requires strategic financial management. Professional accounting support helps businesses:

-

Stay updated with tax regulations

-

Maintain accurate financial records

-

Avoid penalties and errors

-

Optimize tax efficiency legally

With expert support, compliance becomes structured and stress-free.

Why Early Preparation Gives You an Advantage

Businesses that prepare early for corporate tax compliance gain a significant advantage. They are better positioned to:

-

Avoid last-minute filing pressure

-

Maintain financial transparency

-

Improve cash flow planning

-

Build stronger financial systems

Preparation is not just about compliance—it’s about control.

Final Thoughts

Corporate tax compliance in Dubai is no longer optional—it is a fundamental part of doing business in the UAE. While the transition may feel challenging, it also presents an opportunity to build stronger financial systems and improve business credibility.

The real question is not whether your business will comply—but whether it is prepared to do so efficiently and accurately.

With the right systems, processes, and professional support, corporate tax compliance becomes less of a burden and more of a structured path toward financial stability and long-term success.